Tags

Asymmetrical, Bonuses, CEO-to-worker pay ratio, destructive meme, Dodd-Frank, Employees, Incentives, Inequality, Retained Earnings, SEC, Shareholders, Taxes

Remuneration can take many forms, but in the end it’s a question of “Show me the money!” as Rod Tidwell so succinctly puts it in “Jerry Maguire”. Both CEO pay packages and financial traders bonuses have grown so large in the last 20 years that they threaten the stability of the social contract.

In the context of inequality I have recently posted about the level of remuneration of the highest paid people in the US, where it is estimated that in 2011 the top 15,837 families had incomes of AT LEAST $8.0 million (including realized capital gains) but actually AVERAGING $23.7 million[1].

The US now mandates that companies reveal just how great that level of inequality is, by publishing the difference between the pay of CEOs and that of workers[2]. But because the Securities and Exchange Commission (SEC), which is meant to say how the requirement would be implemented has not yet bothered to write the rules, almost three years later we still have no CEO-to-worker pay ratios published. Furthermore a number of the largest companies in the US are actively lobbying against the requirement in an attempt at least to water it down.

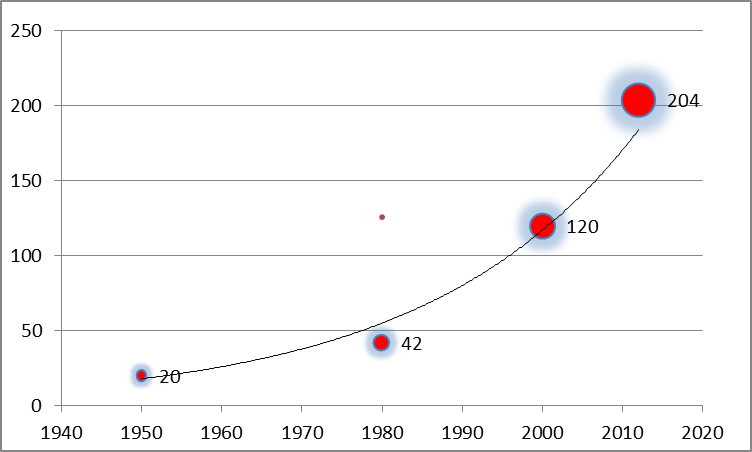

Both Bloomberg[3] and the AFL/CIO[4] have done their own calculations[5]. In both calculations the numbers are quite massive, and the gap has increased more than 10-fold since 1950. The graph below shows how that ratio has progressed (exponentially) since 1950, though it hides the fact that the ratio is significantly lower today than at its peak just before the start of the crisis. A more detailed measure (and commentary) can be found here.

Progression of the CEO to Worker Pay Ratio since 1950

(The circle areas reflect the ratio, and the dot in the middle is about 4 times the representative worker’s base)

Just to add insult to injury, there seems to be no relationship between high pay and high performance. Indeed recent research has shown that, in the words of the Harvard Business Review blog :

“If shareholders think a CEO has done something good to boost profits, they reward the boss with a pay increase amounting to 48.9% (on average) of the perceived contribution to higher profits. But when the CEO is seen as causing a profit decline, there’s a zero effect on his or her pay, Lucian A. Taylor of The Wharton School reports from his study of more than 4,500 chief executives.”[6]

We should also note that it is not only CEOs who earn extremely large sums: part of the underlying (and social) debate on the background to the financial crisis that still blights large parts of the globe was the level of bonuses in financial companies, especially to dealers.

In particular, it was notable how often extremely large pay-offs were based on present profits which seemed to have been booked without taking into account any hidden (or often quite visible!) future risky liabilities incurred in creating that profit. To translate that last sentence into plain English, let us illustrate with an example: suppose an insurance underwriter takes in a much greater amount of premium than last year by selling many more insurance policies, and, in doing so, also gains market share from competing companies…. It would look at first sight as though s/he deserves some special recompense for doing such a great job, no? But what if the only reason that business increased so much was because the policies were sold too cheaply? And what if on top of that a number of the policies go catastrophically wrong, resulting in pay-outs many many times the size of the TOTAL premiums gathered? The underwriter would have been paid a bonus based on present performance, with no account taken of possible future disaster resulting from that very “performance”. And THAT is exactly what happened at AIG[7] as well as in a number of other places! So all too often the hope of receiving inordinately large bonuses provided perverse and asymmetrical incentives to take risk with other people’s money, where you win big if you get it right (often as much by luck as by skill); but you lose little (and often not even your job) if you get it wrong. That kind of incentive is a form of moral hazard.

So what is to be done? The first step is to realise that change will not occur swiftly, nor should it be mandated or enshrined in law in any way. The move towards the perverse idea that the sole purpose of a quoted company is to maximise shareholder value (in the restricted sense that value here only gets measured in terms of dollar profitability, or worse, in the share price) is a relatively recent one and took many years to take root. And it will take many years to uproot it. What is most important in this context is the triumph of ideas, not the enforcement of laws: no law mandates that maximising shareholder value should be the purpose, let alone the sole purpose, of a quoted company.

What is needed is a deeper understanding of the purpose of a company, and how that purpose fits into the structure of a civilised society. That understanding has to be nurtured and promoted, repeated to all and sundry and consciously propagated, until it takes root in society in general, and in the financial and political world in particular, just as that incredibly destructive meme about shareholder value has managed to parasite itself on the rest of us.

What form might this understanding take?

I have discussed this over many years with many colleagues, friends and acquaintances, including many who still hold to the old meme, and the following is the distillation of the conclusions we have usually ended up with.

There are four other constituencies that have a claim on a company’s earnings/profits. They are :

The shareholders: shareholders do, after all, “own” the company, and may legitimately feel that they have a right to at least some of the company’s profits.

The employees: any given employee may well be replaceable (even the ridiculously overpaid CEO or massively overbonused trader). But the employees as a whole are essential. They should therefore expect to get paid, and to be paid fairly relative to other employees of the same company.

The taxman: all companies require the basic infrastructure provided by the society within which they work, whether that infrastructure comes in the form of a framework within which the law of contracts is upheld and enforced; or in more practical ways such as the maintenance of the roads used to transport the company’s products. There are a myriad ways in which taxes support the business of all and any company, and they are often ignored. We may wish to argue about whether we get value for money for our taxes, but we undoubtedly could not continue for long without any of what is provided (whatever the more rabid believers in free-markets or in libertarianism may believe in their wetter dreams).

The company itself! : Yes, the company itself has a right to expect that some of the earnings it has created should be ploughed back into it, whether in the form of R&D, to expand the range of future products, or in the form of the amortisation (and therefore eventual replacement) of equipment et al, or in the form of physical or geographical expansion of the company’s operations. A company should legitimately expect a significant portion of earnings to be retained as an investment in the company’s future.

How do we translate the existence of these four worthy constituent parts of a company’s ability to create wealth and profit, into a structure of how that wealth and profit should be distributed? And how does that structure itself get translated into action by companies?

My suggestion is that any discretionary remuneration (i.e. bonus over and above basic salary) should be considered unacceptable if it ever totals more in any year than the total that the company in the same year pays 1] in dividends to its shareholders, 2] in total ordinary payroll to its employees 3] in total taxes to local and other government, and 4] what the company retains in earnings (i.e. invests in itself).

Any translation we agree upon needs to become a social meme, an accepted truth, and the goal is two-fold: to banish forever the concept that maximising shareholder value is the sole purpose of a company; and to make it completely unacceptable for bonuses of any kind to breach the basic four limits described above, in letter or spirit.

[1] Of course it’s not all wages/salaries (or even S Corporations)… but it is remuneration

[2] Section 953(b) of the Dodd-Frank Wall Street Reform and Consumer Protection Act

[5] The difference between their two averages probably derives from the fact that the union’s calculation is based on only 327 of the Fortune 500 companies, whereas Bloomberg seems to have used all 500

[6] Good News Boosts the CEO’s Pay; Bad News Has No Effect. For more detail see Lucian Taylor’s paper : CEO Wage Dynamics: Estimates from a Learning Model

[7] Some may wish to argue that there is a difference between CDS and insurance…. And there is, but not enough to obviate the point that I am making.